Novo vs. Lilly: Do Mega-Caps Need Strong Leaders—or Strong Governance?

Dave Ricks proves it quarterly. Lars Rebien Sørensen proved it a decade ago. Which mandate wins?

One of Europe's Greatest Corporate Success Stories

Novo Nordisk transformed diabetes care. Ozempic and Wegovy turned obesity into one of the fastest-growing pharmaceutical markets in history. By 2024, Novo Nordisk was Europe's most valuable listed company. Few European companies have created comparable value for patients, shareholders and society.

This was no accident.

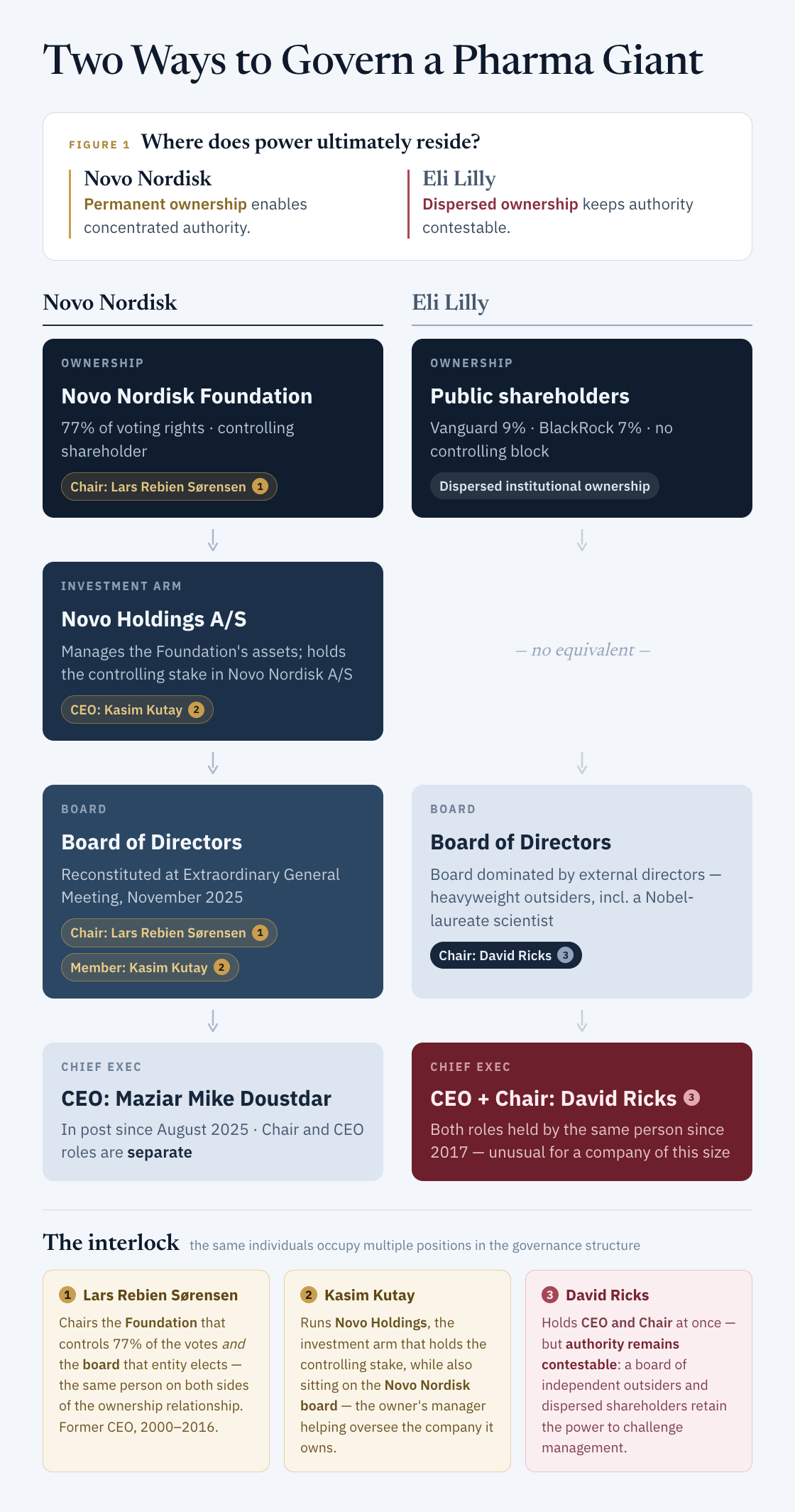

Unlike almost every other global mega-cap, Novo Nordisk has never answered primarily to quarterly capital markets. Behind the company stands the Novo Nordisk Foundation, which controls roughly 77% of the voting rights through Novo Holdings. For decades, that ownership structure insulated management from hostile takeovers, activist investors and the pressure to maximize the next quarter's earnings. It allowed Novo to pursue a consistent scientific strategy while much of the pharmaceutical industry diversified, restructured or chased the next fashionable therapeutic area.

For years, the model appeared almost impossible to criticize.

Then, remarkably quickly, the story changed.

When Success Stopped Compounding

The first cracks appeared in December 2024.

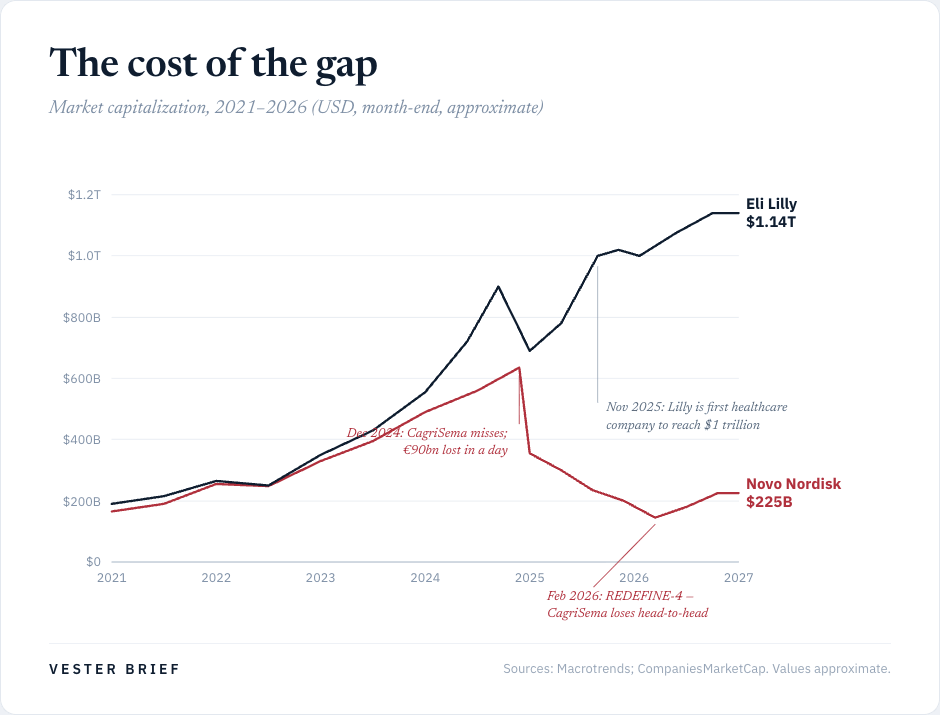

CagriSema, Novo's next-generation obesity therapy and the product expected to drive much of the company's future growth, disappointed in a pivotal Phase III trial. Patients lost 22.7% of body weight, well below the roughly 25% management had guided investors to expect. Novo lost about €90 billion in market value in a single day.

Within months, Lars Fruergaard Jørgensen was gone.

His successor, Maziar "Mike" Doustdar, had joined Novo as an office clerk in Vienna in 1992 and spent more than three decades rising through finance, operations and international leadership. By any measure, another Novo insider.

Within weeks of taking over, Doustdar announced 9,000 layoffs at a restructuring cost of DKK 8 billion. Senior commercial executives departed. Doustdar himself warned investors that performance would decline before improving.

Then came another setback. In February 2026, REDEFINE-4 showed that CagriSema fell short of Eli Lilly's tirzepatide (23.0% vs 25.5%) in a head-to-head Phase III trial. Barclays cut its peak sales estimate for the drug from $12 billion to $2 billion, while a series of analysts downgraded the stock.

There were genuine positives. Oral Wegovy exceeded expectations, Novo remained the market leader in total U.S. GLP-1 prescriptions, and guidance was modestly improved.

But the central fact remained: the problems did not leave with the CEO.

The Obvious Suspect

If one person symbolized Novo Nordisk's governance, it was Lars Rebien Sørensen.

He led Novo Nordisk as CEO for sixteen years, overseeing one of the greatest periods of value creation in European corporate history. He never fully left: since 2018 he has chaired the Novo Nordisk Foundation, and until November 2025 also Novo Holdings, its controlling investment vehicle. That month, he handed Novo Holdings to Lars Green — another Novo veteran — and took the chairmanship of Novo Nordisk itself. One man now chairs both the top of the pyramid and the operating company at its base.

To many governance observers, the diagnosis seems straightforward. The operating company is chaired by its former CEO. The controlling shareholder is chaired by a man whose entire career ran through the Novo system.

Corporate governance research has long warned about precisely these arrangements. In one of the field's landmark studies, Quigley and Hambrick (2012) examined 181 CEO successions at high-technology firms and found that when former CEOs remain as board chairs, their successors exercise significantly less strategic discretion. They divest fewer businesses, reallocate fewer resources and replace fewer executives. More strikingly, a retained predecessor constrains upside more than it cushions downside — precisely the wrong trade-off for a company that needs to recapture lost ground, not protect existing gains.

Rebien differs from their subjects in one respect: he did not stay on as chair, he came back — nine years later, through the ownership structure. If anything, that sharpens the concern. A predecessor who lingers casts a shadow; one who returns has been handed the company.

Rebien himself has acknowledged the awkwardness. "I am well aware that my presence on the board is on sufferance," he has said publicly. "It is for a short number of years." His own description underscores that he views the arrangement as temporary rather than permanent.

He looks like the obvious suspect. If the story ended there, it would be a familiar one: the towering predecessor who came back.

The Story Is Older Than Lars Rebien

There is just one problem with that explanation.

It assumes Novo's governance changed when Lars Rebien became chairman. It didn't.

Long before Lars Rebien assumed his current roles, Novo followed essentially the same governance philosophy. Sten Scheibye chaired Novo Nordisk before later chairing Novo Holdings. Lars Rebien followed the same path, and when he left Novo Holdings in 2025 to become chairman of Novo Nordisk, he was succeeded there by Lars Green.

The pattern was not completely uninterrupted. After Scheibye stepped down in 2013, the chair passed to two external chairmen with no Novo executive background — Göran Ando, then Helge Lund — a twelve-year interlude. Yet it proved temporary. In late 2025, the Foundation once again entrusted the chairmanship to a former Novo CEO.

The individuals changed. The institutional logic did not.

That distinction matters. Replacing one individual is relatively easy. Changing a governance philosophy built over decades is something else entirely. Novo did not become continuity-oriented because of Lars Rebien. Rather, Lars Rebien emerged from a system that has consistently valued stability, institutional memory and long-term stewardship.

What appears at first to be the influence of one individual increasingly looks like the character of one institution.

The contrast with Carlsberg is revealing. Faced with the same governance debate, Denmark's other major foundation-controlled company chose the opposite direction. Since 2022, Carlsberg Foundation chair Majken Schultz has deliberately reduced the Foundation's direct presence in Carlsberg's governance.

"If I look inward, I've said one thing: it will never happen on my watch. The alternative to stepping in yourself is replacing the chair. I would never do it myself. It would be a dramatic step backwards for all the governance work we have just completed."

— Majken Schultz, Chair, Carlsberg Foundation

If one wanted to design a governance model that maximized continuity, it would be difficult to improve on Novo's. The question is whether continuity remains the capability Novo needs most.

The contrast becomes clearer when viewed alongside Eli Lilly.

Two Strong Boards, One Difference

Neither governance model is textbook.

At Lilly, David Ricks has combined the roles of CEO and chair since 2017 — precisely the concentration of authority that governance codes traditionally discourage. Yet that concentration is balanced by a board composed largely of heavyweight outsiders: sitting and former CEOs, leading scientists such as Nobel laureate Carolyn Bertozzi, and directors whose careers were built outside Lilly. Most importantly, the board ultimately answers to dispersed shareholders. If investors lose confidence, they retain the ability to replace directors, challenge management or support activist campaigns.

Novo's board has also become considerably stronger. The 2026 AGM brought in Helena Saxon, Jan van de Winkel and Ramona Sequeira, adding significant external experience in life sciences, investment and global pharmaceuticals. The board has broadened.

But the ownership architecture has not.

Those directors were nominated by the Novo Nordisk Foundation, whose board is now chaired by Lars Rebien Sørensen. The operating company is chaired by the same former CEO. Lilly concentrates authority in management while retaining external mechanisms capable of challenging it. Novo concentrates authority in the permanent owner itself.

Markets do not price governance directly. They price the consequences of governance. Today those consequences are reflected in a valuation gap of roughly five to one between Lilly and Novo Nordisk (as of July 2026). The question is how much of that gap ultimately reflects different capacities to adapt.

The Governance Problem Has Changed

The Foundation solved one of the hardest problems in corporate governance: it gave Novo the freedom to pursue a scientific strategy that ultimately transformed diabetes and obesity care. Without that structure, Novo might never have become Novo.

But success changes the governance problem. For three decades, Novo's greatest challenge was resisting short-term pressure from financial markets. Today's challenge is different. The company no longer needs patience to discover GLP-1 medicines. It needs speed to respond to a competitor that currently appears ahead on efficacy, commercial execution and pipeline renewal.

So the question is no longer whether the model worked; it clearly did. The question is whether an architecture built for continuity can produce discontinuity — and here Rebien's own timeline is part of the problem. Three years is a governance clock. The market runs on a competitive one: orforglipron launches, formulary negotiations, pipeline read-outs measured in quarters. Lilly's powerful CEO faces a referendum every ninety days; Novo has given itself until 2028.

The obesity market will not wait for Danish governance to complete its transition. By the time Rebien hands over the chair, the question he was installed to answer may already have been decided — in Indianapolis.

If you found this useful, forward it to one colleague who enjoys thinking about corporate governance.

Next Tuesday: The Wall Street Banks' Best Exports

References

[1] Quigley, T.J. & Hambrick, D.C. (2012). “When the Former CEO Stays on as Board Chair: Effects on Successor Discretion, Strategic Change, and Performance.” Strategic Management Journal, 33(8), 834–859. https://sms.onlinelibrary.wiley.com/doi/10.1002/smj.1945

Data & Press Sources

• Novo Nordisk Foundation board: https://novonordiskfonden.dk/en/who-we-are/our-board/

• Novo Nordisk Annual Report 2025 — Board of Directors: https://annualreport.novonordisk.com/2025/governance/board-of-directors.html

• CEO succession announcement (May 2025): https://www.globenewswire.com/news-release/2025/05/16/3082984/

• CEO appointment — Doustdar (July 2025): https://www.pharmexec.com/view/novo-nordisk-maziar-mike-doustdar-president-ceo

• Novo 9,000 layoffs & restructuring: https://www.fiercepharma.com/pharma/novo-nordisk-lay-9000-workers-new-ceo-aims-save-13b-year-late-2026

• Chairman Helge Lund resignation (Fortune): https://fortune.com/2025/10/21/novo-nordisk-helge-lund-chairman-resigns-board-changes/

• Foundation board takeover (BioSpace): https://www.biospace.com/business/novo-foundation-replaces-pharmas-board-revealing-deep-divisions-over-leadership

• CagriSema head-to-head loss (CNBC): https://www.cnbc.com/2026/02/24/novo-nordisk-nvo-stock-lilly-lly-cagrisema-zepbound-buy-sell.html

• Wegovy pill Q1 2026 beat (CNBC): https://www.cnbc.com/2026/05/06/wegovy-glp1-weight-loss-novo-nordisk-earnings-stock-nvo-ozempic.html

• Eli Lilly 2025 Proxy Statement (SEC): https://www.sec.gov/Archives/edgar/data/0000059478/000005947825000107/lly-20250321.htm

• Novo Holdings board changes: https://www.prnewswire.co.uk/news-releases/novo-holdings-to-make-changes-to-its-board-of-directors-302590222.html

• Carlsbergfondet chair on Novo governance (Børsen): https://borsen-dk.esc-web.lib.cbs.dk/nyheder/perspektiv/carlsberg-ejers-forperson-om-rebiens-traek-jeg-ville-aldrig-gore-det